Traditional Saudi banks advertise competitive SAR to INR exchange rates but bury 3-7% in hidden fees that slash your family’s rupee payout. Correspondent bank charges, processing fees, and wide spreads compound across international remittances, making digital wallets suddenly appear far cheaper. Indian expats lose thousands of rupees annually to these undisclosed costs.

SAR to INR fluctuates between 22-25 rupees per riyal daily, but banks ensure you never see mid-market rates. This breakdown reveals exactly what they don’t disclose during branch visits or mobile banking.

SAR to INR Transfer Costs Explained

SAR to INR converts Saudi Riyal to Indian Rupee through SWIFT networks connecting SAMA-regulated banks to RBI-partnered Indian counterparts. Each hop extracts fees while applying unfavorable exchange rates versus live mid-market benchmarks.

- Mid-market rate (XE.com): Your true SAR/INR benchmark.

- Bank spread: 2-4% worse than live rates (never advertised).

- SWIFT fees: SAR 50-150 deducted in India, invisible to sender.

- Processing: SAR 20-50 flat regardless of transfer size.

Hidden Fees Traditional Saudi Banks Charge

Al Rajhi, SNB, NCB, and Riyad Bank quote attractive SAR to INR rates but layer multiple charges that compound against expat remitters supporting families back home.

Expert Tip: Always ask for “total INR receipt amount” before processing, banks resist showing this because it reveals 5-8% effective costs versus digital alternatives.

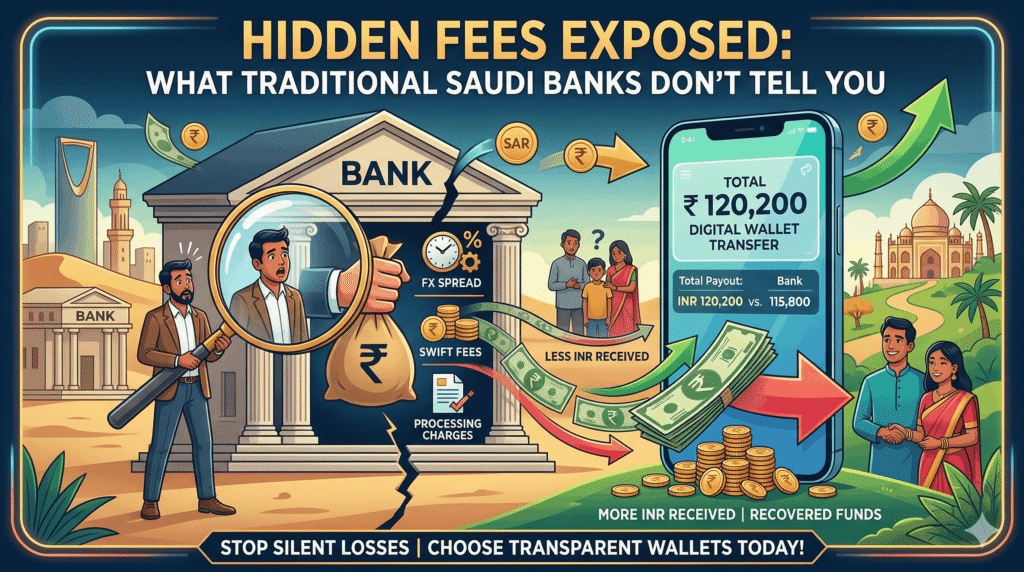

Conversion Example

Mid-market: SAR 5,000 = 121,250 INR at 24.25 rate. Bank quotes “24.10 rate” but after SAR 75 SWIFT + SAR 25 processing + 2.5% spread, recipient gets 115,800 INR. You lose SAR 225 (4.5%) silently.

Fee Breakdown By Major Saudi Banks

- Al Rajhi Bank: SAR 30 processing + SAR 75-100 correspondent + 3% spread = 5.8% total cost.

- Saudi National Bank (SNB): SAR 50 flat + variable “partner bank fee” (SAR 80 avg) + 2.8% spread = 5.2% total.

- Riyad Bank: SAR 40 service + SAR 120 max SWIFT + 3.2% spread = 6.1% effective rate penalty.

- NCB (NCB Payibbar): SAR 25 processing + SAR 90 India fees + 2.5% spread = 4.9% total cost.

- All banks: Weekend transfers add 0.5-1% spread widening automatically.

Hidden Fees Saudi Banks Don’t Disclose

Beyond obvious charges, traditional banks embed costs during SAR to INR processing that erode your intended family support.

- Correspondent deduction: Partner banks (ICICI, HDFC) skim SAR 75 before INR conversion.

- FX spread: Advertised “24.20 rate” hides 24.20 BUY rate vs 23.50 SELL rate you receive.

- Weekend markup: Friday/Saturday spreads widen 1% automatically.

- Intermediary banks: 2-3 hops x SAR 20-30 each = SAR 60+ unshown.

- Currency rounding: Leftover SAR 4.75 “held for compliance” never returns.

Digital Wallets vs Bank Hidden Fees

UrPay/STC Pay show total INR payout upfront, SAR 5,000 typically yields 120,200+ INR vs banks’ 115,800. Wallets eliminate SWIFT/intermediary fees entirely.

- Wallet total cost: 1-2% spread only, transparent preview.

- Bank total cost: 5-7% layered charges, final INR obscured.

- SAR 10,000 monthly difference: SAR 500+ saved via wallets.

- Annual impact: SAR 6,000+ recovered for 12 transfers.

Protect Yourself From Hidden Fees

Verify every SAR to INR transfer shows exact INR receipt before confirming. Demand fee breakdown from bank staff, most won’t provide until challenged. Digital wallets display complete math upfront, eliminating guesswork.

Stop Bank Hidden Fees Today

Hidden fees exposed reveal traditional Saudi banks cost 3-7% more than advertised SAR to INR rates through layered charges expats rarely notice. Switch to wallets showing final INR payouts, test with SAR 100 first, then scale savings monthly. Every riyal recovered compounds into meaningful family support back home.